What We See

Unlocking Value and Maintaining Discipline in a Rapidly Expanding Asset Based Finance Market

November 2025

Overview

Asset Based Finance (ABF) is now one of the most exciting segments within private credit, drawing increased attention from both investment firms and capital allocators. While the strategy’s growth potential is widely recognized with many new entrants joining the space, few market participants are positioned with the flexibility and discipline required to unlock its full value. The solution: dynamic and adaptive investing.

This approach to investing leverages broad capabilities and disciplined capital deployment, resulting in the ability to continuously capitalize on persistent sources of excess spread across the enormity of ABF markets. Long-term shifts in wholesale funding that began after the Global Financial Crisis, now accelerated by near-term catalysts and new market entrants, have created a particularly compelling window of opportunity. At the same time, as new capital and new structures enter the market, differences in underwriting standards, transparency, and structural protections are becoming more pronounced — heightening the importance of disciplined and flexible capital allocation.

Dynamic Investing in Asset Based Finance

Dynamic credit investing in ABF relies on two core principles: maintaining a broad investment toolkit across the ABF universe and exercising discipline in continuously deploying capital to the most attractive risk-adjusted returns. This flexible mandate across sectors, sizes, and structures enables investors to consistently uncover and exploit inefficiencies that traditional lenders and narrowly focused credit managers often overlook.

Several enduring structural features of ABF markets make them especially well-suited for a dynamic approach, particularly for investors with deep credit expertise and the capacity to navigate complexity. These include:

- A vast and structurally complex market: ABF spans a wide range of sectors and structures, including Residential, Commercial, Consumer, and Specialty Finance sectors, creating a market that is difficult to categorize and often inaccessible to conventional credit capital. We estimate this market exceeds $12 trillion in size.

- Lack of standardization: The bespoke nature of ABF, combined with limited transparency and inconsistent reporting, legal frameworks, and asset definitions, makes risk assessment highly nuanced. These challenges are especially pronounced outside the U.S., where jurisdictional complexity further fragments the market.

- Persistent reputational overhang: Despite improved fundamentals and underwriting standards since the 2008 financial crisis, parts of the ABF market remain tainted by legacy perceptions. This has discouraged many institutional investors, leaving significant portions of the market underappreciated and underserved.

Together, these factors create a structurally inefficient financing environment. As banks and other traditional capital providers continue to retreat from large segments of the real asset space due to regulatory pressure and past market shocks, the opportunity for skilled, non-bank lenders to step in has grown increasingly attractive.

Recent Trends Have Created Increased Inefficiencies

In recent years, record amounts of capital have been raised to pursue opportunities in ABF, much of it within narrowly focused, sector-specific vehicles. As a result, flexibility and a go-anywhere investment mandate have become more important than ever—not only for uncovering overlooked or underappreciated sectors, but also for actively avoiding overcrowded areas of the market.

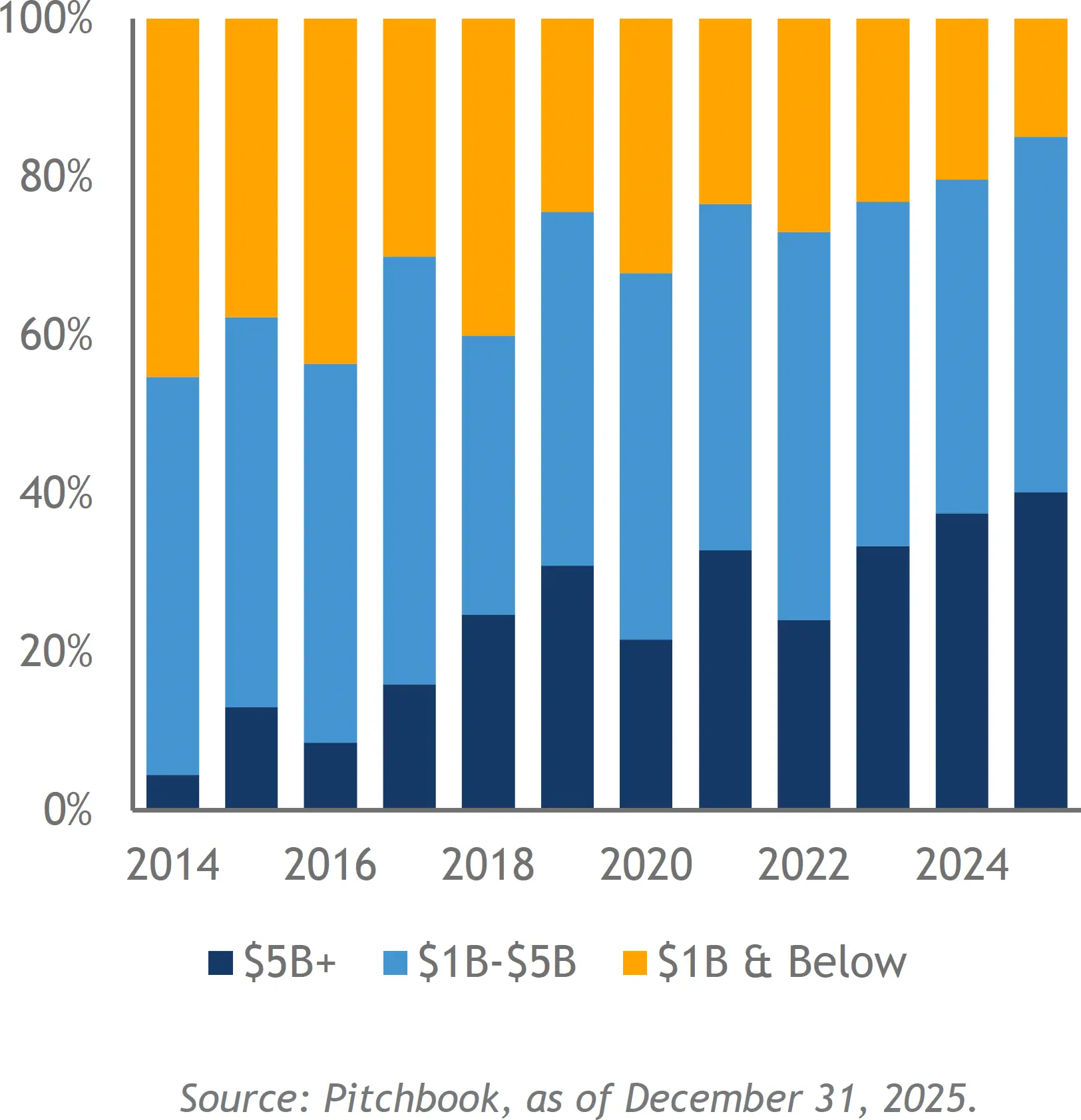

While there is a perception that size is essential to accessing the most attractive opportunities, the data suggests otherwise. Over 85% of private debt capital raised last year went into funds with more than $1 billion in AUM, creating intense pressure to deploy capital into a limited number of “mega-transactions.” This has led to diseconomies of scale, where an abundance of capital drives down returns rather than enhancing them.

Private Debt Capital Raised by Fund Size

A recent example is the competitive bidding process for a nearly $1 billion auto loan portfolio, which attracted significant attention due to its size. Despite the operational complexity including thousands of underlying borrowers and the need for sophisticated infrastructure, the portfolio ultimately priced at tight levels, less attractive than smaller, comparable portfolios. Similar dynamics have emerged in recent multi-billion-dollar French and U.S. mortgage pool sales, as well as large unsecured consumer credit forward flow agreements, where scale did not translate to better pricing or value.

In this environment, the ability to remain agile — targeting more nuanced, less-contested opportunities — is a clear advantage in delivering superior risk-adjusted returns.

Seizing the Opportunity with Flexibility

Dynamic investing is at the heart of Sculptor’s approach to ABF. Since 2007, this philosophy has underpinned nearly $50 billion of investments across the ABF universe, including Residential, Commercial, Consumer, and Specialty Finance assets. Our adaptive nature enables us to evaluate opportunities across the full market spectrum, without the constraints inherent in more narrowly defined strategies.

This flexibility allows us to focus solely on sourcing transactions that offer compelling excess spread, without rigid allocation targets across sectors and opportunities. By staying nimble and selective, we consistently identify niche, complex, or underappreciated opportunities that lie outside the focus of more traditional or specialized lenders. Many of these transactions are either too small, too intricate, or too unconventional for larger market participants to pursue effectively.

We retain full discretion over our investment decisions, including when and where we allocate capital. Our approach is designed to ensure that sourcing and investment decisions remain closely aligned allowing us to remain focused on the most compelling risk-adjusted returns. The result is a flexible and dynamic deployment model that adapts to shifting market conditions, sector, acquisition strategies, and structures.

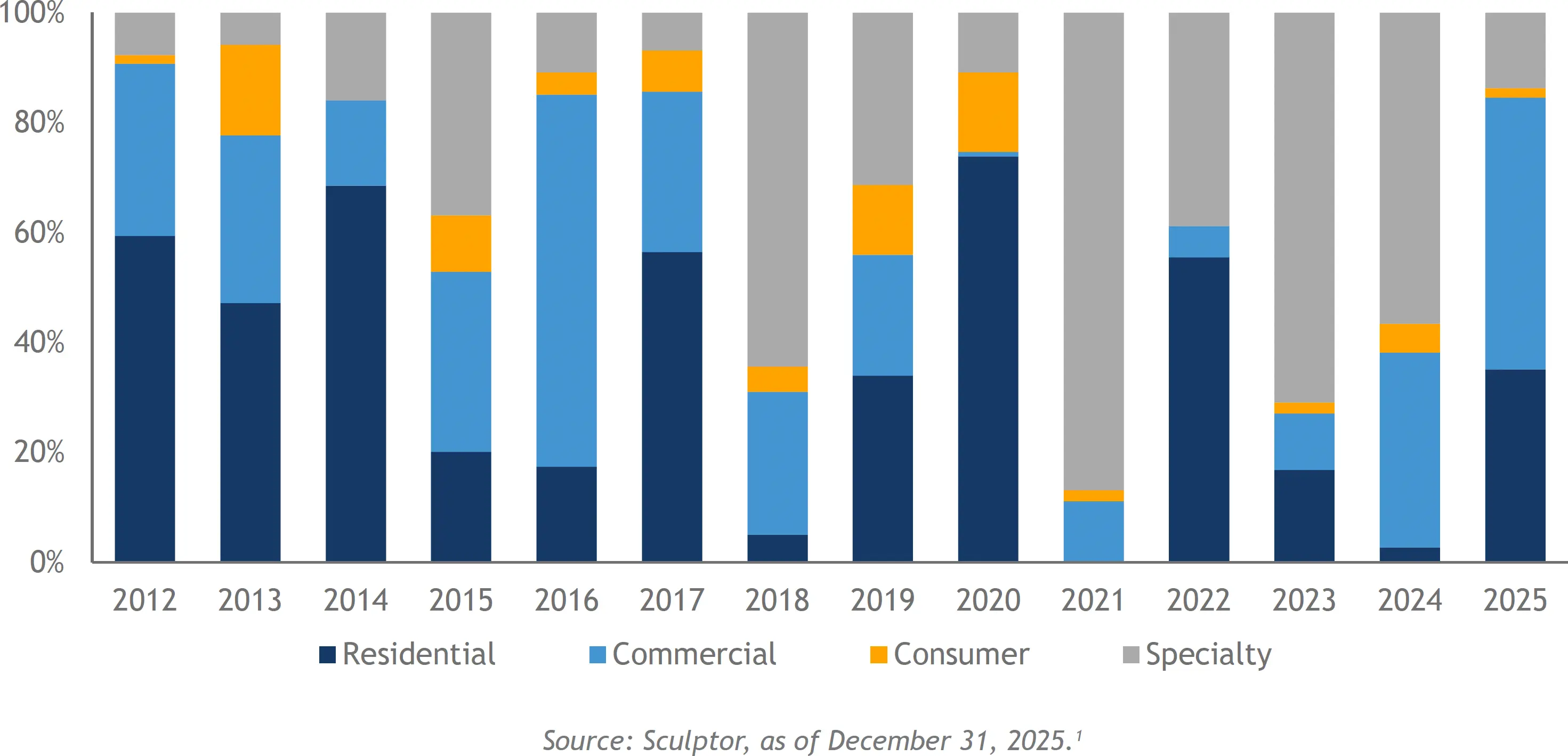

Historical Capital Deployment by Asset Type

A Track Record of Flexibility in Action1

Our investment history in the chart above clearly demonstrates that we are not anchored to any single sector, rather, we go where the opportunity is most attractive. The 2020–2022 period provides a vivid example of this philosophy in practice:

- 2020: As the COVID-19 pandemic disrupted global markets, we rapidly pivoted into Residential mortgages — driven by conviction in a housing recovery, strong borrower fundamentals, and historically wide spreads. While others hesitated, we acted early and decisively. Residential assets accounted for nearly 75% of our capital deployed that year, up from just roughly 35% in 2019.

- 2021: As spreads tightened and Residential valuations surged, the opportunity became less compelling. Rather than chase returns dependent on leverage and ultra-low funding, we shifted toward bespoke and structurally complex investments, especially in Specialty Finance. Activity in Residential dropped to near zero, while Specialty Finance rose from roughly 10% to nearly 90% of our deal volume. Investments included secured hard asset finance, SRT transactions, and dislocated aviation-related assets—where returns were driven by structural features, not spread compression.

- 2022: With interest rates spiking and securitization markets stalling, we returned to Residential — but in a very different form. We financed portfolios of stranded mortgage assets, acquiring deeply out-of-the-money deals with strong downside protection. Though reliant on the same underwriting discipline, these transactions required significantly different structuring approaches to unlock value. This evolution was not an anomaly: it exemplifies our consistent approach to ABF. As market trends shift, we adapt. Across Residential, Consumer, Commercial, and Specialty Finance sectors, our allocation strategy evolves in response to risk-reward conditions, sourcing frameworks, and transaction complexity. We believe our ability to underwrite across sectors, source off-market opportunities, and structure around complexity is central to unlocking long-term value in ABF markets and remains a core differentiator of our platform.

Narrowbody Aviation2

Aviation financing changed drastically during COVID. Previously a well-capitalized space supported by a deep bench of public securitization market participants, the pandemic drove a sharp pullback that resulted in both equity and debt financing sources abandoning the midlife sector. Geopolitical conflicts and global economic concerns have further added to these challenges. With a robust recovery in global passenger traffic, an undersupplied new aircraft market, and desires for fleet modernization, what once was primarily an ABS driven market is now vastly underserved. Given our extensive activity in aviation over a near twenty year investing history, including serving as the exclusive asset manager for a worldwide leader in aviation financing, we were able to analyze not only the capital shortage in the midlife space, but also the fundamental shortage in aircraft metal confronting airlines. Ongoing production and performance issues related to new aircraft deliveries have supported midlife aircraft valuations, making it our preferred corner of the market. Since the Russian invasion of Ukraine, new issuance of aviation ABS debt has remained dormant while higher benchmark rates and wider spreads have led many aircraft owners to warehouse assets or seek alternative financing. Although ABS spreads began tightening in 2023, overall financing costs remained elevated. This created a window to target high-yield, unlevered opportunities on a selective basis. Capitalizing on these conditions, our activity was elevated in 2024 within the Specialty Finance sector. One transaction that contributed to this broader focus was the acquisition of a midlife Airbus A320 aircraft on lease to a wholly-owned subsidiary of one of the world’s premier airlines based in Asia. The aircraft had originally been aggregated alongside other aircraft pre-COVID by its owner in anticipation of a public securitization. However, the 2022 rate hiking cycle and broader macro uncertainty further suppressed demand for aviation ABS, stalling the transaction. By late 2023, the seller had failed to reach sufficient scale for a securitization and began to offload individual assets. We saw an opportunity to acquire the aircraft at a historically wide yield relative to comparable aviation assets and broader credit instruments, supported by highly attractive pricing, limited financing options in the market, and, in our view, a fundamental misunderstanding of the credit risk of the lessee. The leaseholder benefits from the financial strength of its parent company, which has ample cash on its balance sheet, limited debt and an implicit credit backing from the government. Despite improving sentiment at the time, many lessors remained constrained by elevated funding costs, allowing us to transact at an attractive yield, with upside tied to potential spread tightening and improvement in lease rates and residual value of the metal.

Key Pillars Enabling Dynamic Investing Within an Expansive Asset Class

In a market characterized by limited transparency and structural fragmentation, analytical depth, sourcing reach, and disciplined execution are essential to executing on this strategy.

- Proprietary Data & Analytics: In ABF, access to meaningful data is often the defining edge. Investors must rely on proprietary performance data, historical analogs, and sophisticated cash flow modeling to assess true relative value. At Sculptor, we have developed purpose-driven technology and analytics infrastructure since 2007 to meet this challenge. Our proprietary platform includes extensive market and asset-level data, much of it is unavailable through third-party providers, enabling precise underwriting with deep contextual insight. This platform also allows for cross-asset comparison across diverse structures, helping us to consistently identify investments with the strongest risk-adjusted returns.

- Consistent and Active Market Presence: Sculptor’s longstanding presence across all ABF verticals has established our reputation as a trusted counterparty. These relationships with both specialist and generalist originators grant us consistent access to complex, time-sensitive, and off-market opportunities. Importantly, our approach is to remain actively engaged in sourcing and underwriting even during quieter deployment periods. This ensures pricing and structuring discipline is maintained while preserving market access, rather than stepping away and risking disconnection. As market conditions shift, this continuous presence enables agile capital reallocation to the most compelling risk-reward opportunities.

- Disciplined Investment Framework: Every investment at Sculptor is evaluated within a defined and multi-layered risk management process. Opportunities undergo detailed analysis by the investment team, rigorous vetting by the investment committee, and independent validation by our risk and analytics groups. This framework ensures that capital is only deployed into situations we deeply understand, and only when the risk-reward profile is clearly favorable.

Maintaining Discipline Amidst Surging Demand for ABF Assets

While these pillars have guided our approach since 2007, their importance has only intensified as ABF has evolved into one of the most competitive segments within private credit. As the market expands and investment approaches diversify, we have witnessed the range of structures categorized as “asset based” broaden meaningfully. This evolution has created an expanded opportunity set, but also greater variation in how risk is viewed, evaluated, and monitored.

Drawing upon our near-two decades of ABF history, our experience has reinforced two core principles that underpin successful asset based lending:

- Collateral valuation and cash-flow characteristics must be grounded in verifiable data and aligned with realistic recovery expectations, especially in stressed scenarios.

- Ongoing performance monitoring is essential, with frameworks designed to detect changes early enough to enable thoughtful action.

In today’s rapidly growing environment, we observe that the application of these principles can vary widely across participants. This is a natural consequence of an asset class attracting new capital and new entrants, each bringing different datasets, underwriting philosophies, and monitoring infrastructures. Certain structural nuances can materially influence outcomes and, in our view, warrant heightened scrutiny.

Non-Contractual or Unsecure Cashflows

Structures that rely on cashflows without clear contractual support or without bankruptcy-remote protections can present challenges in stressed outcomes. For example, certain factoring and reverse-factoring arrangements, while useful for specific situations, may blur the line between operating exposure and isolated collateral exposure. Recent bankruptcies have illustrated how intertwined cashflows can reduce recoveries, even when headline structures appear robust.

Similarly, transactions with borrower populations exposed to concentrated economic or policy sensitivities may behave differently from model expectations. In one high-profile instance, our diligence identified inconsistencies between reported loss performance and broader industry data, as well as borrower characteristics that could present challenges in the current environment. These conclusions did not align with our risk tolerance, and we chose not to participate. In cases such as these, small differences in assumptions can compound significantly in execution.

Loose Cash Account Control

Even when cashflows prove collectable, an additional structural consideration is control over the accounts through which those cashflows are remitted. Reliance on borrower-controlled cashflows can weaken creditor protections. Delayed remittance, commingling of funds, and limited visibility can impair a lender’s ability to respond as performance deteriorates. By contrast, structures incorporating lender or third-party controlled cash accounts, lockbox arrangements, or deposit account control agreements help ensure that contractual rights translate into practical control. Effective cash account governance remains a key consideration alongside asset and cashflow quality, monitoring, and enforcement protections.

Forward-Flow Consumer Structures

Consumer forward-flow programs have grown in prominence, driven by the desire for predictable deployment and stable returns. As participation has broadened, we have observed growing variations in credit-boxes, verification methods, and loan modification practices. These differences can influence reported performance trends. For instance, while headline delinquency rates appeared to stabilize in 2023, a closer look revealed that it was driven largely by loan modifications including “skip-a-pay” features, and forbearance programs. These interventions suppress delinquencies and obscure true performance.

We have selectively engaged only where data transparency was strong, assumptions were conservative, and pricing clearly aligned with downside protection. In other cases, we opted to be opportunistic rather than stretch for transactions, recognizing that a rapidly growing market often requires patience for performance patterns to normalize.

Collateral With Limited Practical Recoverability

Another area where we see increasing dispersion is the treatment of collateral whose theoretical value may differ from its practical recoverability. Certain residential solar finance structures are a good example. While often marketed as secured consumer assets to prime borrowers yielding double-digit returns, a $30,000 solar system may have only $5,000–$10,000 of used value before removal costs which can exceed $10,000. The cost and complexity of repossession may reduce the economic value of the claim. In these circumstances, even high-quality borrowers may not fully mitigate recovery difficulties. This does not diminish the opportunity within solar loans but rather underscores the need to align underwriting with the asset’s real-world liquidation characteristics.

Conclusion

ABF sits at the intersection of long-term structural inefficiencies and near-term market changes. The post-GFC regulatory environment, shifting bank priorities, and a higher rate backdrop have created a fertile environment for private capital. As capital continues to flow into the space, however, differences in structure, data transparency, underwriting rigor, and monitoring approaches have widened the dispersion of outcomes—particularly in strategies where historical performance data is limited or structural assumptions play an outsized role.

We believe this dispersion is likely to become more pronounced over time. In a growing and increasingly competitive market, dynamic investing provides a distinct edge: the ability to allocate capital flexibly toward the most compelling risk-adjusted opportunities while avoiding areas where underwriting discipline, structural protections, or recovery assumptions may erode.

Navigating this evolving landscape requires independence, analytical depth, and unwavering adherence to fundamentals—grounded in verifiable collateral values, realistic recovery expectations, and active performance oversight. These principles have guided us through multiple market cycles and position us to deliver capital solutions that are durable for borrowers and reliable for clients as the ABF market continues to mature.

Important Disclosures & Appendix

Important Information

The information contained in this document is presented to inform decisions to use Sculptor Capital LP as an investment adviser, should be treated as confidential, and may not be shared with others absent the written consent of Sculptor Capital LP.

As of May 2026, unless otherwise noted. Certain statements made herein reflect the subjective views and opinions of Sculptor and its personnel. Such statements cannot be independently verified and are subject to change. Past performance is not a reliable indicator of future results

This material is provided to you for informational purposes only. This is neither an offer to sell nor a solicitation of any offer to buy any securities in any fund managed by Sculptor Capital LP, and its affiliates (collectively, “Sculptor Capital Management,” the “Firm,” “Sculptor,” or the “Company”). This Financial Promotion has been issued or approved for distribution in the United Kingdom by Sculptor Capital Management Europe Limited, a member of the Company. Sculptor Capital Management Europe Limited is authorised and regulated by the Financial Conduct Authority (Registration No. 190662). Any offering is made only pursuant to the relevant offering documents and the relevant subscription application (collectively, the “Offering Documents”), all of which must be read in their entirety. The information contained herein will be superseded by, and is qualified in its entirety by reference to, the Offering Documents, which will contain information about the investment objectives, terms and conditions of the relevant investment fund and will also contain tax information and risk disclosures that are important to any investment decision regarding the relevant investment fund. No offer to purchase securities will be made or accepted prior to receipt by the offeree of these documents and the completion of all appropriate documentation. This material does not constitute investment advice and does not create any advisory relationship; such a relationship may only be established through a formal advisory contract. This document is not intended for public use or distribution. The information contained herein should be treated in a confidential manner and may not be reproduced or used in whole or in part for any purpose, nor may it be disclosed, without prior written consent of the Company. Notwithstanding anything to the contrary herein, each investor (and each applicable employee, representative, or other agent of each such investor) may disclose to any and all persons, without limitation of any kind, the tax treatment and tax structure of (i) the Fund and (ii) any of its transactions, and all materials of any kind (including opinions or other tax analyses) that are provided to the investor relating to such tax treatment and tax structure.

The figures and calculations contained herein were internally generated by Sculptor based on estimated data and analysis. These figures and calculations have not been audited or otherwise confirmed by a third party. Returns are stated in U.S. Dollars and may increase or decrease as a result of currency fluctuations – please refer to important disclosures in the Appendix. Additional important disclosures regarding region-specific regulatory requirements (e.g., the European Union’s Sustainable Finance Disclosure Regulation (“SFDR”)) and disclosures required by the National Futures Association regarding Digital Assets will be included in the Offering Documents.

While private investment funds offer investors the potential for attractive returns and diversification, they pose greater risks than more traditional investments. Investors’ capital is at risk and investors may lose all or a substantial portion of their investment. Investors should consider the risks inherent with investing in private investment funds, which include, but are not limited to, leveraged and speculative investments, limited liquidity, higher fees and expenses and complex tax structures. The tax treatment of any investment will depend on the individual circumstances of each investor and may be subject to change in the future.

The Company has in place policies and procedures designed to prevent market abuse and insider dealing. These policies and procedures are reviewed on a regular basis.

- Past strategy allocations and exposures are not necessarily indicative of future allocations and exposures.

- The investment example contained herein (the “Case Study”) is being provided for information purposes only and is not intended to be and should not be considered a recommendation to purchase or sell any security or to invest in any fund managed by Sculptor. The Case Study was selected by Sculptor using non-performance based criteria as a representative example of the investment themes discussed herein. The Case Study is not presented (and was not selected) on the basis of performance. There can be no assurance that any Case Study or any actual account would realize its investment objectives or be profitable. Furthermore, there can be no assurance that any future investments will be realized at a profit, and any investment could lose all or a substantial portion of its value.

Cautionary Note Regarding Forward-Looking Statements

Certain information contained in this herein constitutes “forward-looking statements” that can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “target,” “project,” “estimate,” “intend,” “continue,” or “believe” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results or the actual performance of any Firm investment may differ materially from those reflected or contemplated in such forward-looking statements.

Risk Factors

The following considerations, which summarize some, but not all, of the risks of investing in the Funds managed by Sculptor and its affiliates should be carefully evaluated before making an investment in a Fund. The information set forth under “Risk Factors” in a Fund’s Confidential Memorandum must be reviewed in its entirety prior to investing in a Fund. An investment in a Fund will involve significant risks, including the loss of the entire investment. Any interests in the Funds will be illiquid, as there are no secondary markets for interests in the Funds and none are expected to develop.

Dependence on Sculptor. The success of the Funds is dependent upon the ability of Sculptor to manage the Funds and effectively implement the Funds’ investment programs. The Funds’ governing documents do not permit the limited partners to participate in the management and affairs of the Funds. If the Funds managed by Sculptor were to incur substantial losses or were subject to an unusually high level of redemptions or withdrawals, the revenues of Sculptor may decline substantially. Such losses and/or redemptions/withdrawals may impair Sculptor’s ability to provide the necessary level of service to the Funds as it has in the past and continue operations. The loss of the services of Sculptor could have a material adverse effect on the Funds and the limited partners’ investments therein.

General Economic and Market Conditions. The success of the Funds’ activities will be affected by general economic and market conditions, such as interest rates, availability of credit, credit defaults, inflation rates, economic uncertainty, changes in laws (including laws relating to taxation of the Funds’ investments), trade barriers, currency exchange controls, and national and international political circumstances (including wars, terrorist acts or security operations). These factors may affect the level and volatility of the prices and the liquidity of the Funds’ investments. Volatility or illiquidity could impair the Funds’ profitability or result in losses. The Funds may maintain substantial trading positions that can be adversely affected by the level of volatility in the financial markets. A downturn in the relevant financial markets may occur at any time, which could result in a deterioration in the financial condition of various parties.

Investment and Due Diligence Process. Before making investments, Sculptor will conduct due diligence based on the facts and circumstances applicable to each investment. When conducting due diligence, Sculptor may be required to evaluate important and complex business, financial, tax, accounting and legal issues. When conducting due diligence and making an assessment regarding an investment, Sculptor will rely on the resources reasonably available to it, which in some circumstances, whether or not known to Sculptor at the time, may not be sufficient, accurate, complete or reliable. Due diligence may not reveal or highlight matters that could have a material adverse effect on the value of an investment.

General Credit Risk. The issuers of debt instruments may face significant ongoing uncertainties and exposure to adverse conditions that may undermine the issuer’s ability to make timely payment of interest and principal. In addition, major economic downturns and financial market swings have adversely affected, and could in the future adversely affect, the ability of some of the issuers of such instruments to repay principal and pay interest thereon and may increase the incidence of default for such instruments.

Leverage and Financing Risk. It is expected that some or all of the Funds will leverage their capital. Accordingly, the Funds may pledge their securities and may provide other forms of security or assurance in order to borrow additional funds for investment purposes. The Funds also may leverage their investment returns with derivative instruments. The amount of borrowings which the Funds may have outstanding at any time may be large in relation to their capital. Leverage has the effect of potentially increasing losses. Accordingly, any event which adversely affects the value of an investment by a Fund would be magnified to the extent the Fund is leveraged. The cumulative effect of the use of leverage by a Fund in a market that moves adversely to the Fund’s investments could result in a substantial loss to the Fund.

Non-U.S. Securities. Investments in securities of non-U.S. issuers (including non-U.S. governments) and securities denominated or whose prices are quoted in non-U.S. currencies pose, to the extent not hedged, currency exchange risks (including blockage, devaluation and non-exchangeability) as well as a range of other potential risks which could include expropriation, confiscatory taxation, imposition of withholding or other taxes on dividends, interest, capital gains, other income or gross sale or disposition proceeds, limitations on the removal of funds or other assets of the Funds, political or social instability or diplomatic developments that could affect investments in those countries.

Liquidity of Investments. The Funds may acquire securities that are traded only among a limited number of investors. The limited number of investors for those securities may make it difficult for the Funds to dispose of those securities quickly or in adverse market conditions. Some markets in which the Funds may invest may prove at times to be insufficiently liquid or illiquid. The Funds may invest in securities which are subject to legal or other restrictions on transfer or for which no liquid market exists. The market prices, if any, for such securities tend to be volatile and the Funds may not be able to sell them when they desire to do so or to realize what they perceive to be the fair value of the securities in the event of a sale. Furthermore, there is a risk that, because of a lack of liquidity and efficiency in certain markets due to unusual market conditions or unusually high volumes of repurchase requests or other reasons, the Funds may experience some difficulties in purchasing or selling holdings of securities and, therefore, meeting subscriptions and withdrawals in the time scale indicated in the Funds’ Confidential Memorandums.

Distressed Investment Risk. The Funds may invest, directly or indirectly, in securities of U.S. and non-U.S. issuers in weak financial condition, experiencing poor operating results, having substantial capital needs or negative net worth, facing special competitive or product obsolescence problems, or that are involved in bankruptcy or reorganization proceedings. Investments of this type may involve substantial financial and business risks that can result in substantial, or at times even total, losses. Among the risks inherent in investments in troubled entities is the fact that it frequently may be difficult to obtain information as to the true condition of such issuers. Such investments also may be adversely affected by laws relating to, among other things, fraudulent transfers and other voidable transfers or payments, lender liability and the bankruptcy court’s power to disallow, reduce, subordinate or disenfranchise particular claims.

PAST PERFORMANCE IS NOT A RELIABLE INDICATOR OF FUTURE RESULTS. INVESTMENTS ARE SUBJECT TO A RISK OF LOSS AND INVESTORS MAY LOSE ALL OR A SUBSTANTIAL PORTION OF THEIR INVESTMENT.

IMPORTANT NOTICE: JURISDICTIONAL SELLING LEGENDS AND RELATED DISCLOSURES WILL BE CONTAINED IN THE FUND’S CONFIDENTIAL PRIVATE PLACEMENT MEMORANDUM, WHICH SUPPLEMENTS THE INFORMATION CONTAINED HEREIN AND IS REQUIRED TO BE REVIEWED BEFORE MAKING A DECISION TO INVEST IN THE FUND. RULES AND REQUIREMENTS GOVERNING SECURITIES OFFERINGS MAY VARY AND ARE BASED ON A VARIETY OF CIRCUMSTANCES, INCLUDING THE JURISDICTION WHERE AN OFFER IS MADE.